Episode 84: How Can I Prepare for IRS Changes in 2023?

Planning for IRS changes in 2023

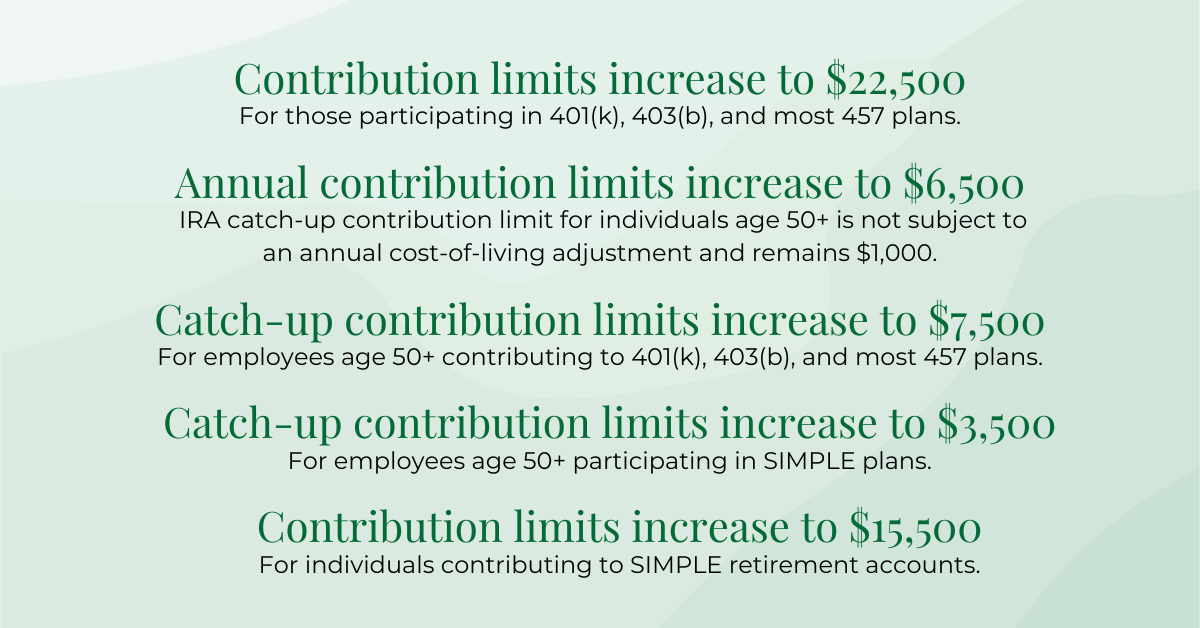

There are relevant and very important changes for those focusing on retirement planning to know. Due to inflation, the IRS has increased the contribution limits in retirement plans such as 401(K)s, 403(B)s, 457s, and some others, from $20,500 to $22,500 for everyone. If you’re over 50, they’ve increased it from $6,500 to $7,500. If you are over 50 and have the income, you can set aside as much as $30,000 tax-free into your 401(k) plan. That’s a big advantage that inflation has given us with the IRS tax code changes.

Adjusted Tax Brackets

Another change is adjusted brackets. The tax rates haven’t changed, but the brackets have broadened. Visually, you can imagine the buckets that hold certain amounts of money have gotten bigger. So, we all paid the same taxes on the same amounts of money as we go up through the income scale. Everybody pays 10 – 12% on the same amounts of money. The IRS has made those buckets about 7% larger.

In essence, all of us in 2023 will end up paying less taxes on our money. That doesn’t mean tax rates have changed. It means the brackets have gotten a little bit bigger, holding a little bit more money, which lowers our tax bill. If you’re saving into a retirement plan at work and you’re not able to meet the maximum amount of contribution limits, even making a small change that fits your goal and your desired retirement plan may push you into a lower tax bracket with how 401(k) deductions work on your W-2. That is a huge advantage someone can take to maximize their retirement plan and to minimize their taxes. It’s always a win-win when you get to pay less taxes and have more fun in retirement, which really is the goal.

If You’re Already Retired

For those that are already in retirement and are past the saving cycle, be aware that larger tax brackets can allow us to plan for an event, or something expensive, coming up in a few years. Taking the money out to keep ourselves at a lower tax bracket is one way we can maximize tax efficiency in our retirement plan because of these changes.

Roth Conversions

Another exciting way we can maximize tax efficiency is by doing Roth conversions for future planning. This gives us a little more room in the bucket to keep a lower tax rate on the amount that we convert into a Roth. Those are just a couple of ways that the tax changes in 2023 can impact us.

Find A Financial Professional

I just want to encourage you, if you don’t have a financial planner, to find one. It makes all the difference in retirement. Some retirement rules, like these IRS rules, can seem simple on their own, however, keep in mind the two we touched on, and how they interconnect and interrelate to one another is what makes them much more complex. Every person’s plan is different and unique to them. Figuring out how to take all these moving parts and put them together so that they work for you ensures that you can have your best retirement.