What’s the Right Medicare Plan for Me?

There is a lot to consider when choosing the right Medicare plan: How often do you visit the doctor? Do you have any chronic conditions? Do you take prescription drugs regularly? Answering these questions can help you pinpoint the type of coverage you need.

In this week’s Money Wisdom Question Series, join Jake Doser, CFP®, CPWA® as he goes deeper into demystifying key Medicare decisions, starting with the differences between Parts A, B, C, and D.

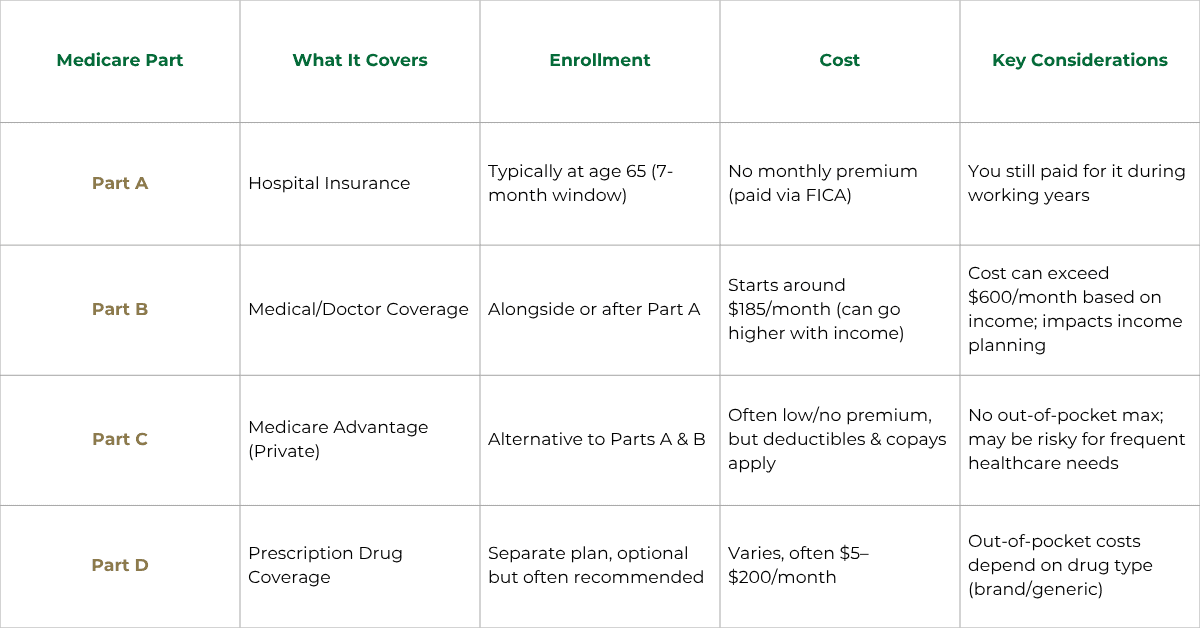

Parts A & B: Original Medicare

Medicare Part A is the initial coverage most people enroll in when they turn 65. You have a seven-month Initial Enrollment Period (IEP) that begins three months before your 65th birthday, includes the month you turn 65, and continues for three months afterward. While there is technically no monthly premium for Part A, you’ve been paying for this coverage throughout your working years via FICA taxes.

Next is Medicare Part B, which, when combined with Part A, is referred to as Original Medicare. Unlike Part A, Part B requires a monthly premium, currently starting at $185 per month. However, if your income exceeds certain thresholds, this premium can increase significantly. That’s why it’s important to include Medicare costs in your overall income planning strategy.

Part C: Medicare Advantage

You also have the option to sign up for Medicare Part C, instead of Parts A & B. Known as Medicare Advantage, these plans often have little to no monthly premium, but they usually include deductibles and copayments.

Additionally, many Medicare Advantage plans do not have a cap on out-of-pocket expenses, so costs can add up quickly. If you have frequent doctor visits or upcoming surgeries, this may not be the best option for you.

Part D: Prescription Drug Coverage

Finally, Medicare Part D is available for prescription drug coverage. Costs for Part D often range from $5 to $200 per month, depending on the medications you need and whether they are brand name or generic. You may also have out-of-pocket expenses based on your prescriptions.

Discuss Your Options with an Agent

It’s important to carefully consider which Medicare plan makes the most financial sense within the context of your overall retirement plan. Working with an independent Medicare agent who understands your options and can provide unbiased advice is crucial. Independent agents have access to a wider range of plans and can help you find the best fit for your needs.

Download Now

10-Point Retirement Checklist

Here’s a checklist of our most important things you can do, to help you retire strong.