Episode 15: Should I Buy Long-Term Care Insurance?

Thank you for joining us for Episode 15 of our Money Wisdom Question Series, where we film answers to common financial and retirement investment questions. Today’s question is “Should I buy long-term care insurance?” It’s a big subject that always comes up and people have a lot of concerns about it.

What is Long-Term Care Insurance?

Long-term care insurance covers you if you need care in your home or in a nursing home. Specifically, it includes a variety of services aimed at helping individuals accomplish the Activities of Daily Living (ADLs). There are varying levels of long-term care dependent upon each person’s assistance level needed.

The Cost of Long-Term Care Insurance

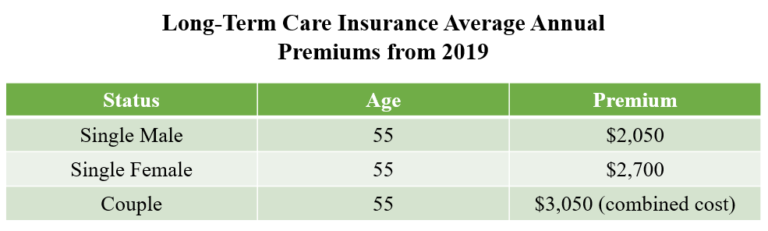

The cost of long-term care insurance does continue to get more expensive and very often, people do say this is a big factor for them. Below is the 2019 Price Index for the average annual premium long-term care insurance. (statistics provided by the American Association for Long-Term Care Insurance)

People will say, “I don’t want to pay insurance for a nursing home.”, but that’s not the reason for purchasing it. It’s to protect your money so that you don’t spend everything on care. If you pass away and didn’t purchase long-term care insurance and ended up having all those medical costs, now there’s no money left for a widow, family, or any other reason that you were saving that money for. It’s expensive because what it insures is very expensive.

What is Your Plan for Long-Term Care?

You don’t necessarily need to buy long-term care insurance, but you do need to have a conversation about what your plan is if you or your spouse gets sick. Your plan could be long-term care insurance. It could be looking at an estate plan or shifting assets out of your name. There are pros and cons to each one of these scenarios. When you look at long-term care insurance, it is a product specifically designed to pay for that need.

Unfortunately, many of us have had grandparents that have been in healthcare facilities. We have had clients that have been in care facilities paying hundreds of thousands of dollars a year. It also depends on the state that you’re living in. For example, here in Connecticut, there is a very high cost of care. You can receive really good care, but it’s expensive.

Don’t Delay

I wouldn’t delay this conversation any longer. Like anything, get a number of different opinions on it. If someone is saying you really need to buy the insurance, think about what is best for you before making that big financial commitment. There are really great options available to you, but make sure to get multiple inputs on them. The most important thing is to have a plan.

Thanks for joining me and I hope you found this information helpful! If you enjoyed this topic and you want to hear more, you’ll love this Forbes article where Joel talks more about long-term care insurance.

P.P.S. Feel free to submit questions here for a chance to have them answered!

Download Now

Estate Planning Checklist

Estate planning is a large component of retirement planning, ensuring your assets are distributed according to your final wishes. Creating an estate plan allows greater control, privacy and security of your legacy.